This analysis provides a comprehensive overview of GE Vernova's current valuation, price target scenarios, and the underlying factors driving its stock performance. The company, spun off from GE in April 2024, has emerged as a leader in the energy transition sector, but questions remain about its sustainable valuation and future growth potential.

Current Valuation (August 2025)

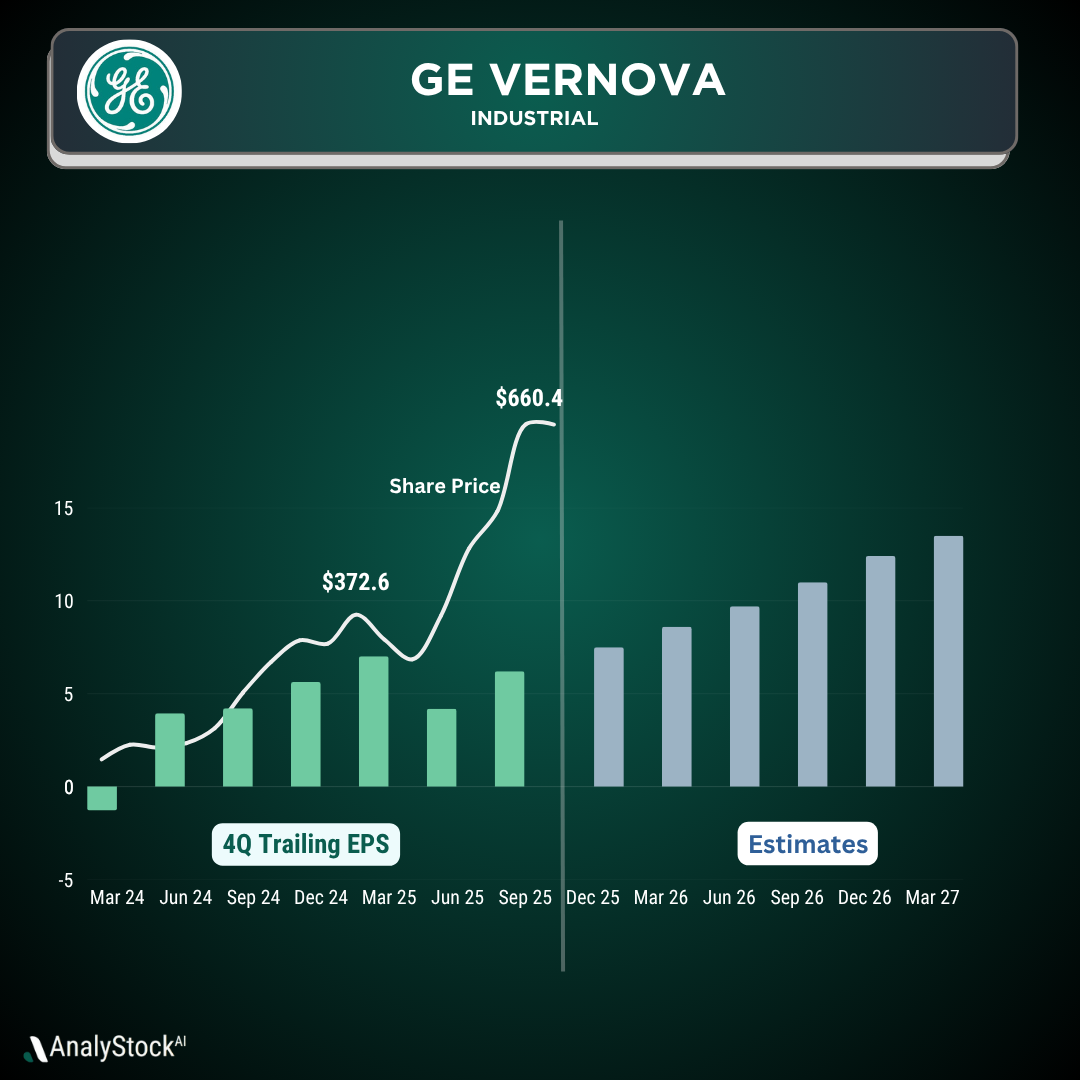

GE Vernova's market cap is approximately $171 billion at around $668 per share, representing a staggering 206% gain year-to-date and over 450% since the spin-off. The stock reached an all-time high of $677.29 in July 2025, up from its post-spin-off low of $115. At current levels, GEV trades at approximately 4.5-5x trailing twelve-month sales (based on ~$36-37B revenue guidance for 2025), which is a premium to traditional industrial companies but reasonable for a growth-oriented energy infrastructure player. On earnings, the stock trades at roughly 30-35x forward P/E based on 2025 estimates, reflecting investor confidence in the company's ability to capitalize on the multi-decade energy transition. Recent quarterly results support this optimism: Q2 2025 revenue rose 12% to $12.4B with EPS of $1.86 (beating forecasts by 24%), while adjusted EBITDA increased 25% to $770M. Free cash flow guidance has been raised to $3-3.5B for 2025, yielding approximately 2% against the current market cap. This modest FCF yield reflects heavy investments in capacity expansion and R&D, positioning the company for the anticipated energy infrastructure boom.

Base Case (12-month view)

Assuming continued execution, GE Vernova could achieve the high end of its 2025 revenue guidance of $37B, with margins continuing to expand across all segments. The company's strong backlog (which has been growing consistently) provides revenue visibility into 2026-2027. With disciplined capital allocation and margin expansion, the company could generate $4-5B in free cash flow by 2026. At a reasonable multiple for a ~15-20% growth business in the energy transition space (say 25-30x earnings), the stock could reach $750-850, representing 12-27% upside from current levels. However, this scenario assumes continued strong execution in power generation, wind energy, and electrification segments. Given the stock's recent run, much of the near-term positive news may already be priced in. A balanced base-case 12-month price target in the range of $700-750 seems reasonable, with upside toward $850 if energy transition momentum accelerates further, and downside to $500-550 if execution disappoints or energy markets soften.

Bull Case (3-5+ years)

In a bullish scenario, GE Vernova becomes the dominant supplier for the global energy transition by 2030. The company is uniquely positioned across multiple growth vectors: renewable energy generation (wind, solar), power grid modernization, energy storage, and gas turbines for backup power. Key bull case drivers include:

- Global Energy Transition Acceleration: $130+ trillion expected investment in energy infrastructure through 2050

- Data Center Power Demand: AI and cloud computing driving massive electricity demand growth

- Grid Modernization: Aging infrastructure requiring wholesale replacement and smart grid technology

- Offshore Wind Expansion: Despite current headwinds, long-term offshore wind market could be massive

- Electrification: Industrial and transportation electrification creating new demand

Under these conditions, GE Vernova's revenue could feasibly reach $60-80B by 2030, with operating margins potentially expanding to 15-20% as the company scales and optimizes its portfolio. This would imply $9-16B in operating income. At a market-average multiple (~20-25x earnings), this would support a $200-400B market cap. If the market continues to assign premium valuations to energy transition leaders (similar to how renewable energy stocks traded during peak enthusiasm), even higher multiples are possible. In an extreme bull case where GE Vernova captures dominant market share in key energy infrastructure segments, a $500B+ market cap is conceivable by 2030, implying a stock price above $1,200 (roughly 80% upside from current levels).

Bear Case

Several risks could derail GE Vernova's momentum:Market-Specific Risks:

- Offshore wind market continues to struggle with supply chain issues, permitting delays, and economics

- Energy transition pace slows due to political changes or economic pressures

- Renewable energy subsidies reduced or eliminated

- Competition intensifies, pressuring margins

Company-Specific Risks:- Execution challenges in scaling operations

- Supply chain disruptions affecting delivery schedules

- Working capital intensity strains cash flow

- Legacy GE operational issues resurface

In a pessimistic scenario where energy transition momentum stalls and GE Vernova faces execution challenges, the stock could see significant multiple compression. Traditional industrial companies trade at 1-2x sales and 12-15x earnings. If GE Vernova's growth slows to mid-single digits and margins compress due to competition, the company might generate only $40-45B in revenue by 2030 with $3-5B in operating income. At a 15x multiple, this would imply a market cap of $45-75B, suggesting a stock price in the $200-300 range (50-70% downside from current levels). A more moderate bear case assumes decent execution but slower market growth, potentially keeping the stock in the $400-500 range over the next 2-3 years as fundamentals catch up to valuation.

Comparables and Relative Valuation

GE Vernova's current profile – mid-teens revenue growth, expanding margins, and exposure to multiple energy megatrends – puts it in a unique category. Few pure-play comparables exist given the company's breadth across power generation, renewables, and grid infrastructure. Relevant Comparisons:

- Siemens Energy: Similar portfolio, trades at ~2-3x sales

- Vestas Wind Systems: Pure wind play, historically volatile valuations

- Schneider Electric: Electrification focus, trades at ~3-4x sales

- Caterpillar: Industrial/energy infrastructure, ~2-3x sales

GE Vernova's 4.5-5x sales multiple reflects a premium to most industrial peers but appears justified by its growth profile and strategic positioning in energy transition. The multiple expansion since the spin-off suggests the market has re-rated the business from a traditional industrial conglomerate to an energy transition growth story. This relative valuation supports the thesis that much of GE Vernova's current value reflects energy transition potential rather than just current fundamentals. If execution falters, there could be significant multiple compression toward peer levels.

Price Target Summary and Analyst Conclusion

Taking these scenarios into account, here are rough price targets for GE Vernova stock:

- 12-month (August 2026): Base case around $700-750 per share, assuming continued strong execution and energy market growth. Upside toward $850 if energy transition momentum accelerates or the company wins major contracts. Downside toward $500-550 if execution disappoints or energy markets weaken.

- 3-year (2028): If GE Vernova executes well on the energy transition opportunity, revenue could reach $50-60B with significantly improved margins. With a growth-oriented multiple (20-25x earnings), the stock could reach $900-1,200 per share. Conversely, if growth disappoints, the stock might trade flat to down in the $400-600 range.

- Long-term Bull vs Bear (2030+): The bull case sees GE Vernova as the dominant energy infrastructure supplier, potentially supporting a stock price above $1,200 if the company captures major market share in key growth segments. The bear case sees significant multiple compression if energy transition momentum slows, potentially taking the stock to $200-400 levels.

Analyst Conclusion: Thesis Recap: GE Vernova is no longer just an industrial spin-off – it's a pure-play on the global energy transition with exposure to multiple high-growth infrastructure segments. Our core thesis is that the world is entering a multi-decade energy infrastructure super-cycle driven by decarbonization, electrification, and digitalization. GE Vernova is uniquely positioned to supply this transformation with its comprehensive portfolio spanning power generation, renewables, and grid infrastructure. With a ~$171B market cap, GE Vernova trades at a premium to traditional industrials but reasonably for a company positioned at the center of energy transition trends. The stock has already experienced massive appreciation, but if the company executes on its energy transition strategy, further upside is possible. The making of an energy infrastructure giant. The reason GE Vernova could continue its strong performance is its combination of strategic positioning and execution capability. This isn't just a momentum play – the company has demonstrated strong operational improvements and is winning in key growth markets. The company has proven it can compete and win against established players (evidenced by its growing backlog and market share gains). If one believes in the secular trend toward renewable energy, grid modernization, and electrification, then GE Vernova stands to benefit from decades of infrastructure investment. However, the stock's remarkable performance has raised valuation concerns. Much of the positive energy transition scenario may already be priced in, making execution critical to justify current levels.