📋 Highlights

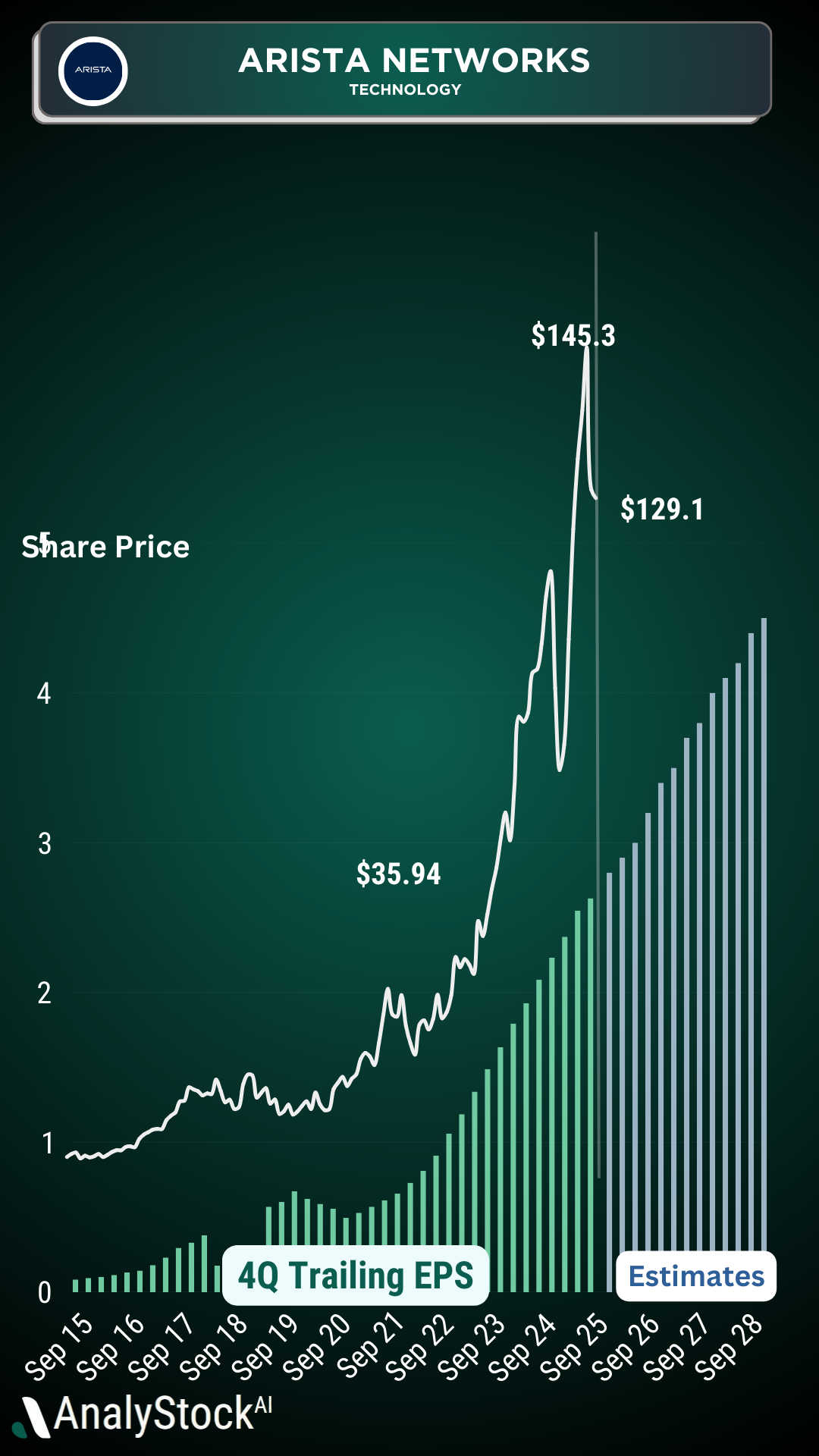

- Strong Revenue Growth Driven by AI Infrastructure: Arista Networks delivered 27.5% YoY Q3 revenue growth ($2.308B) and is on track for $8.87B in 2025 revenue, with AI networking revenue now 26% of total sales and growing at 40-50% annually.

- Attractive Valuation with High Margins & Cash Flow: Despite a 50x P/E ratio, Arista’s 64% gross margin, 39.7% net margin, and $4.05B in TTM free cash flow justify premium pricing, with a PEG ratio of 1.86 indicating reasonable growth-adjusted valuation.

- Competitive Threats from Nvidia & Customer Concentration: Nvidia’s Spectrum-X is rapidly gaining market share (25.9% in Q2 2025 vs. Arista’s 18.9%), and customer concentration (Microsoft + Meta: 40-45% of revenue) creates execution and pricing risks for the company.

- Long-Term Growth Potential in AI Networking: Arista could capture $40-75B in AI-related revenue by 2030 by securing 10-15% of the $400-500B AI data center networking market, supported by its technical moat in open Ethernet and hyperscaler partnerships.

- Key Risks: Margin Compression & Capex Cycles: Gross margins face pressure from product mix shifts and competitive pricing, while hyperscaler capex cycles (historically cyclical) pose a risk of sudden demand contraction in 2027-2028 if AI ROI assumptions prove optimistic.