📋 Highlights

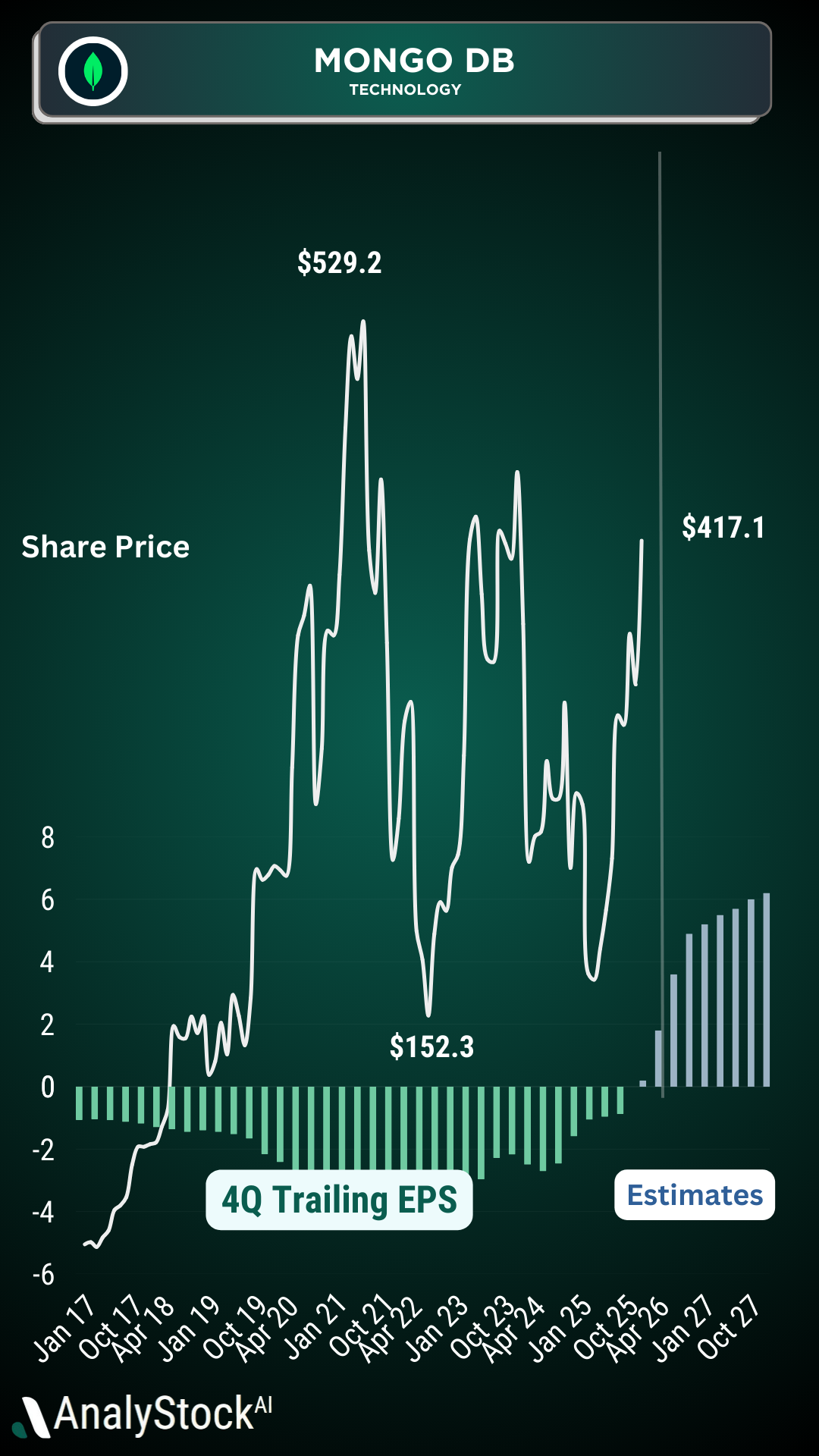

- Strong Q3 Performance and Atlas Growth:: MongoDB reported $628.3M revenue (19% YoY growth) with Atlas accounting for 75% of total revenue and growing 30% YoY, signaling robust cloud-native adoption.

- Leadership Transition:: Chirantan "CJ" Desai, former executives at Cloudflare and Oracle, assumed CEO role in November 2025, bringing cloud infrastructure expertise critical for AI-driven growth strategy.

- High Valuation Metrics:: Traded at ~12× trailing sales and 80× forward earnings, similar to peers like Snowflake, but significantly higher than traditional databases like Oracle, reflecting growth expectations and AI potential.

- AI and Vector Search Momentum:: MongoDB’s vector search capabilities for RAG and AI workflows position it as a key player in the $226B database market by 2028, with 74% of organizations planning to adopt integrated AI databases.

- Guidance Raise and Cash Flow Strength:: Fiscal 2026 revenue guidance increased to $2.434–2.439B (21–22% growth), with Q3 free cash flow of $140.1M, highlighting scalable operations and margin improvement potential.