Company Story

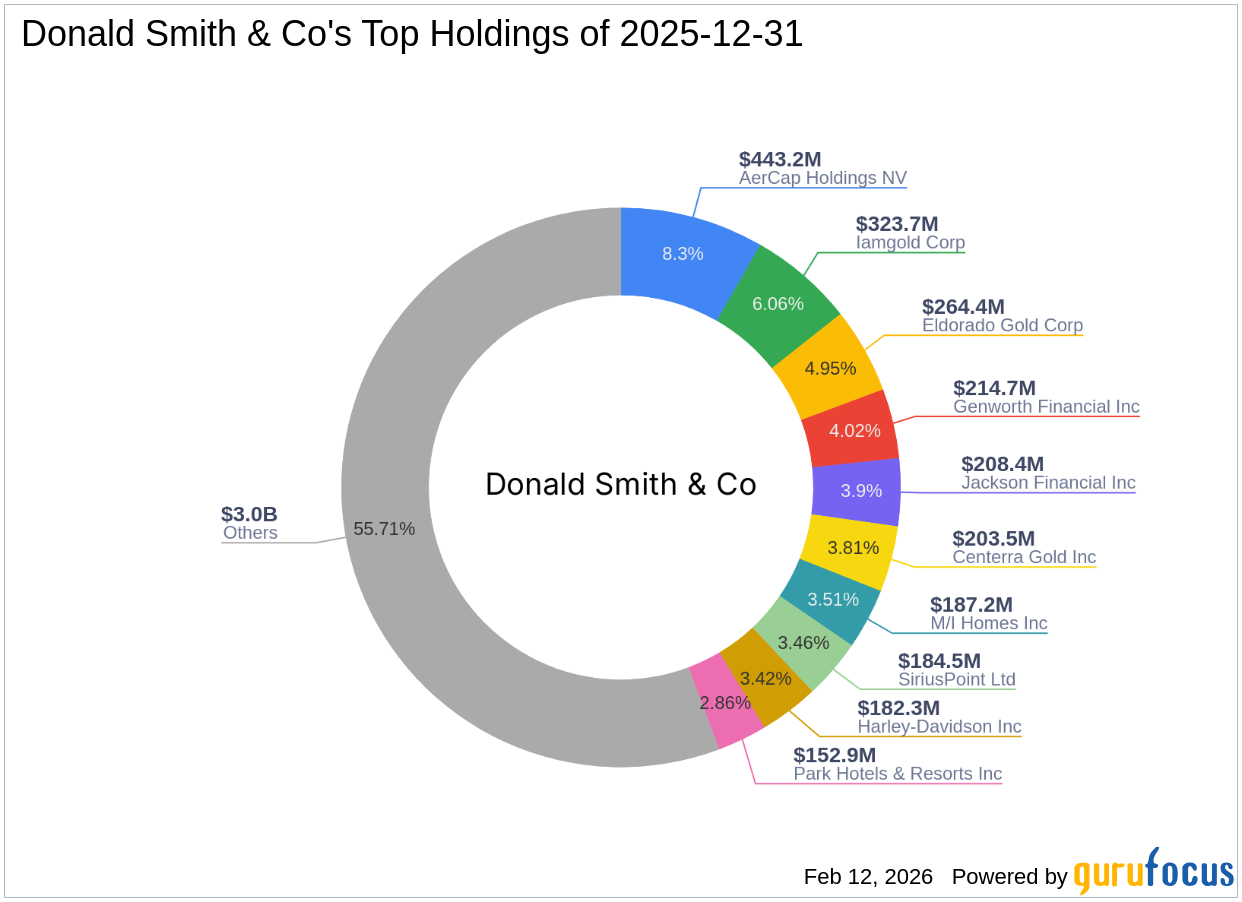

1871 - Genworth Financial, Inc. was founded as The Life Insurance Company of Virginia.

1986 - The company was acquired by Combined Insurance Company of America.

1996 - The company was renamed Genworth Financial, Inc. after a spin-off from Combined Insurance.

2004 - Genworth Financial, Inc. went public with an initial public offering (IPO).

2006 - The company acquired the mortgage insurance business of PMI Corporation.

2012 - Genworth Financial, Inc. acquired the Medicare supplement business of Continental General Insurance Company.

2016 - The company announced a strategic review of its U.S. mortgage insurance business.

2020 - Genworth Financial, Inc. was acquired by China Oceanwide Holdings Group Co., Ltd.